Shilling for ObamaCare Requires One to Willfully Ignore Facts

About a week ago, I wrote about my personal experience with ObamaCare. After the website failures, mangled data, and numerous other problems, the Obama Administration allowed users to see what plans would be available in their area. The sticker shock was unbelievable.

I found among the plans available to my family in my area that it could cost me over $50,000 a year in premiums.

My explanation of the facts was immediately attacked by the Left. The liberals over at the Daily Kos pounced, applauding those on the Left “Bravely taking on Redstate” (where I had originally posted my piece), as commenters from the Left accused me of lying about what I discovered when I went to Healthcare.gov.

Here is one example of a comment from the Left shilling for ObamaCare in an attempt to shout me down.

Please understand that if you currently have health insurance that you like, all you have to do is NOTHING! You can keep that policy for as long as you wish. NO ONE is forcing you to drop that policy to buy an OBAMACARE MARKETPLACE policy.

Clearly, this individual was paraphrasing what President Obama promised the American people on numerous occasions, that “if you like your health care plan, you will be able to keep your health care plan. Period.”

Yet, at this point it requires willful ignorance of the facts to believe these liberal talking points, as they increasingly fall victim to, well, the facts.

Nevertheless, the Daily Kos proudly supported these assertions, stating, “we think these comments are legit.”

Here are a few of the facts. Americans are losing heath insurance under ObamaCare faster than they are enrolling under ObamaCare. Just adding up the reports in the media of insurance companies that have announced they are being forced to drop existing insurance plans for their customers shows that already 1.5 million Americans have lost insurance under ObamaCare. According to NBC News, “50 to 75 percent of the 14 million consumers who buy their insurance individually can expect to receive a ‘cancellation’ letter or the equivalent over the next year.”

We are even learning that the Obama Administration itself has known “for at least three years” now that millions of Americans would lose their health insurance plans.

How did they know, because it is right there in the law and federal regulations, plain as day (45 C.F.R. § 147.140 if you’d like to read it).

Federal regulations (which have been in affect since November 15, 2010) provide that under ObamaCare the “grandfather” clause, allowing you to keep your insurance plan if you like it, is essentially null and void if any of the following instances occur:

- “Elimination of benefits” – i.e. the elimination of one single benefit regarding even one medical condition would end the plan.

- “Increase in percentage cost-sharing requirement” – i.e. if your coinsurance requirement has increased in the slightest since March 23, 2010 (over the past 3 and a half years) the plan would end.

- “Increase in a fixed-amount cost-sharing requirement other than copayment” – i.e. an increase in deductible would cause your plan to be canceled.

- “Increase in fixed-amount copayment” – i.e. if your co-pay has gone up in the last 3 and a half years, the plan will probably fail to be grandfathered.

- “Increase in contribution rate by employers and employees organizations” – i.e. if you have an employer contribution to your health insurance and they went down even slightly, the plan could no longer qualify as a grandfathered plan.

- “Changes in annual limits” – if your plan either had an annual limit placed on it or the annual or lifetime limit decreased in the last 3 and a half years, it wouldn’t be grandfathered.

What health insurance plan hasn’t had one of these changes in the last 3 and a half years?

The Left can keep repeating the same untruth over and over again, but it won’t change the facts. Millions of Americans are losing their health insurance because of ObamaCare.

Faced with the facts, the Left turned to attacking me personally for exposing the outrageous cost of ObamaCare.

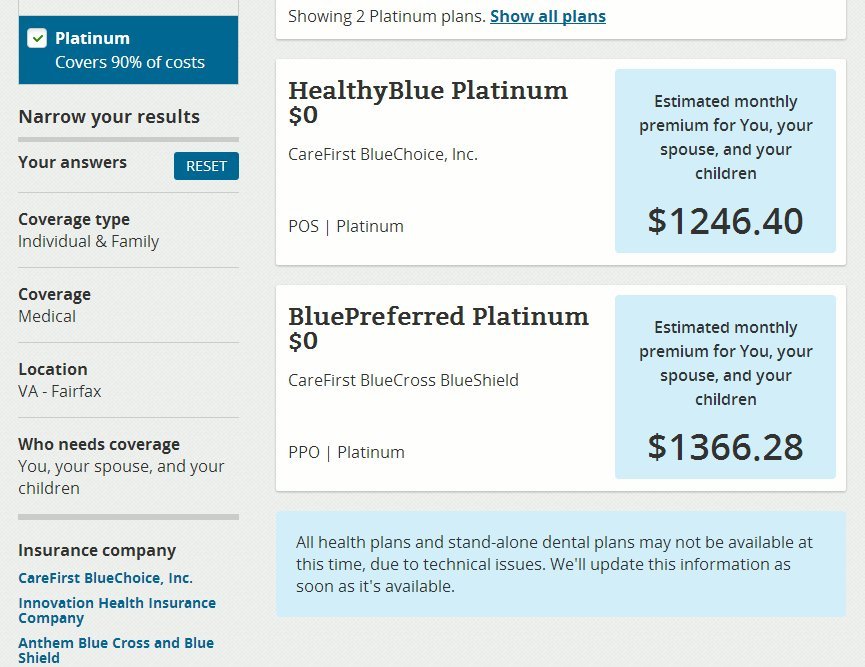

Though I clearly explained exactly how some of the premiums available to me were utterly outrageous (in excess of $50,000 a year), the Left said those weren’t the only plans available. As proof, one commenter clipped a shot of a “cheaper” plan:

I actually want to thank this commenter for clipping this particular plan, because it's a perfect example of the average plan in my area. According to Healthcare.gov, of the 50 plans available to me in my area at all levels (from Catastrophic to Platinum) under ObamaCare, the average plan would cost a family $1,246.28 a month in premiums (Yes, that’s $15,000 a year).

While $15,000 a year in insurance premiums is certainly cheaper than $50,000, if that is what is meant by “affordable” health insurance, then I think the average American family would vehemently disagree.

I just want to point out one final thing. Healthcare.gov does almost nothing to explain what the difference is between any of these plans. I know some plans sound nicer like Platinum than others like Bronze, but the site does nothing to give you any details about what specifically the plans cover or what exactly my out of pocket costs would be.

If confusion, higher costs, and general dysfunctionality was the plan, then ObamaCare has been the success the Left touts. But I doubt the millions of Americans who are losing insurance, can’t get insurance, and are seeing their premiums skyrocket would agree.

If you are one of the millions affected by ObamaCare, sign the petition at ICantEnroll.com to have your voice heard.